Yicheng Wang

Financial Engineer

- BORN : June 25, 1996

- TITLE: Chartered Financial Analyst Candidate

- INDUSTRY : Finance, Technology

- CAREER INTERESTS : Quantitative Risk/Research/Trading or Data Scientist

Since I graduated in May 2019 from New York University Master of Financial Engineering, I worked on some independent projects assigned from companies or online-courseworks. I did web scrapping and data analytics for KKL Solutions LLC. I also worked on some machine learning predictive modeling, credit risk modeling, financial modeling, and trading strategy implementation.

I am familiar with various financial products and programming languages. I have experiences in from retrieving, storing and preprocessing data, to developing quantitative trading strategies of different assets(equity, fixed income, cryptocurrency) in different markets(US, China), to building distributed trading platform, to dealing with trading system.

CFA Level II Candidate, Financial Engineering & Economics Degrees

Data Analysis, Machine Learning, Financial Modeling, Risk Modeling, Algorithmic Trading, Trading System

Excel, Powerpoint, Word, Bloomberg, Tableau, Git, AWS, Google Cloud

Numpy, Scipy, Pandas, SciKit, TensorFlow, Keras, Spacy, Urllib, Sqlalchemy, Flask, BigQuery, Socket, Boto3

PYTHON

SQL

C & C++

EXCEL & VBA

R

MATLAB

Linux Shell Script

PowerPoint & Tableau

Developed market-neutral, medium-frequency Alphas using cross-sectional or time series operations on selected fundamental factors by investigating academic research; Then implemented them on company’s back-testing platform Trexism using Python; Produced high quality reports for share in internal forum;

Grader for: FRE-GY 6831 Computational Finance Laboratory - Python, FRE-GY 6931 Cryptocurrency

Courses: Asset Pricing & Risk Management, Derivatives Pricing, Valuation for Financial Engineering, Stochastic Calculus, Active Portfolio Management, Fixed Income Trading, Quantitative Trading Strategy, Machine Learning

Activities and Societies: Cum Laude; 2017 Economic Honors Program "Outstanding Paper Award" winner

Grader for: Macroeconomics (EBMA course at UW Foster Business School)

Courses: Econometrics, Probability & Statistics, Linear Algebra & Numerical Analysis, Linear & Nonlinear Optimization, Discrete & Continuous Math Modeling, Managerial and Financial Accounting

Activities and Societies: National Honor's Society, Cheerleaders Varsity, Volleyball Junior Varsity, Tennis Junior Varsity

Built Probability Default, Loss given Default and Exposure at Default model using Logistic and Linear Regression; Estimated Expected Loss (Python)

Using various machine learning models to predict whether a company will go bankrupt, using TensorFlow & Sklearn

Implemented a distributed Python platform that could be used to test a quant models (ML) for trading financial instruments in a networksetting under client/server infrastructure

Equity Option Pricing Python Library with Git version control that price European/American/Asian Call/Put and exotic options

The Impact of Earnings Report on Stock Price (C++)

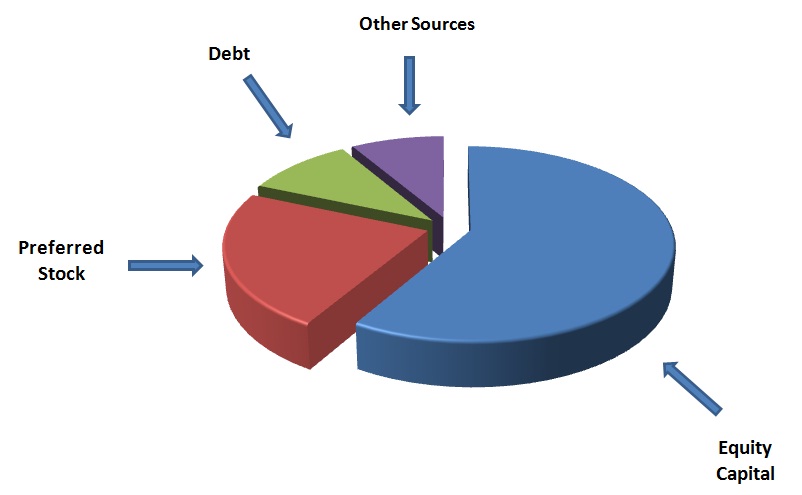

Modelled the cash flow and determined the optimal capital structure of the firm (Excel/VBA)

Yield Curve Fitting & Trading on Weighted Treasury Spreads (Python)

Analyze international debt data by The World Bank; Build ML model to predict the number of rides using BigQuery and dataset from GoogleCloud

Compute factor returns; Constructed Markowitz portfolio and Black and Litterman’s portfolio (Python)

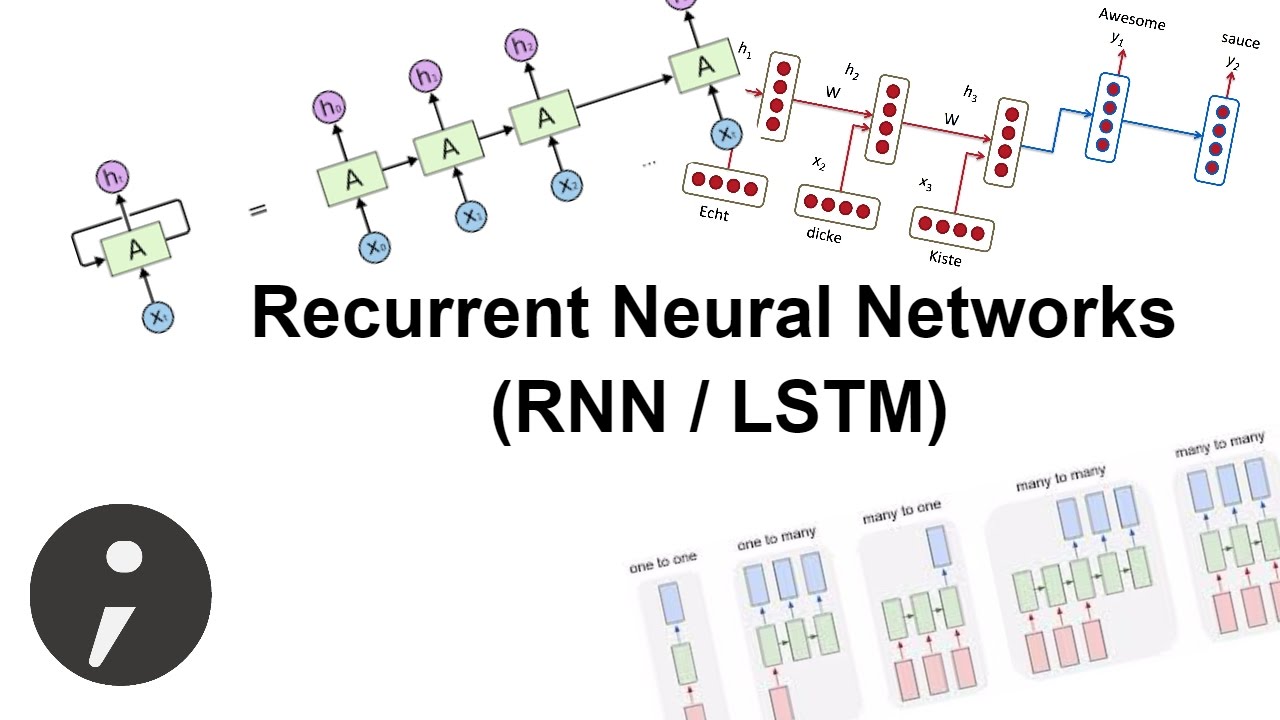

Predict the direction of stock movement from News data and build a long short portfolio using LSTM model (Python)

Researched listing activities on Chinese stock exchanges and the OTC market using econometrics methods (R/Excel)

Analyzed 6 Vanguard indexes; computed Value-at-Risk(VaR) and contructed optimal portfolio (R)